Luxury Brands Face Customer Exodus as Price Increases Reach a Breaking Point

The Shifting Landscape of Luxury Goods: Trends and Challenges Ahead

As we approach 2024, the luxury goods market is poised for a period of stagnation, with demand expected to remain flat at constant exchange rates, according to consulting firm Bain. However, beneath this seemingly stable surface lies a complex and evolving landscape that poses significant challenges for luxury brands. Notably, the sector has experienced a concerning trend: a loss of more than 10% of its usual customer base since 2022, marking the first time in recent memory that the number of luxury shoppers has declined. This shift raises questions about the future of luxury consumption and the strategies brands will employ to navigate these turbulent waters.

The Democratization of Luxury: A Double-Edged Sword

For the past three decades, luxury brands have focused on democratizing their offerings, aiming to attract a broader base of middle-class consumers. This strategy has successfully tripled the size of the luxury market, allowing brands to expand their reach and increase sales. However, recent price hikes have begun to reverse this trend, pushing many potential customers out of the market. The average cost of luxury products has surged since the onset of the pandemic, leading to a significant shift in consumer behavior.

Luca Solca, a luxury-goods analyst at Bernstein, highlights the stark reality of the current market: “Finding regular size [handbags] at less than $3,000 from reputed brands has become virtually impossible.” This price escalation has not only alienated some consumers but has also resulted in a dramatic decrease in the number of products sold. Bain estimates that the luxury industry will see a reduction of 20% to 25% in units sold compared to 2022, with categories like handbags and shoes potentially experiencing a decline of up to a third.

The Price Paradox: Inflation and Consumer Sensitivity

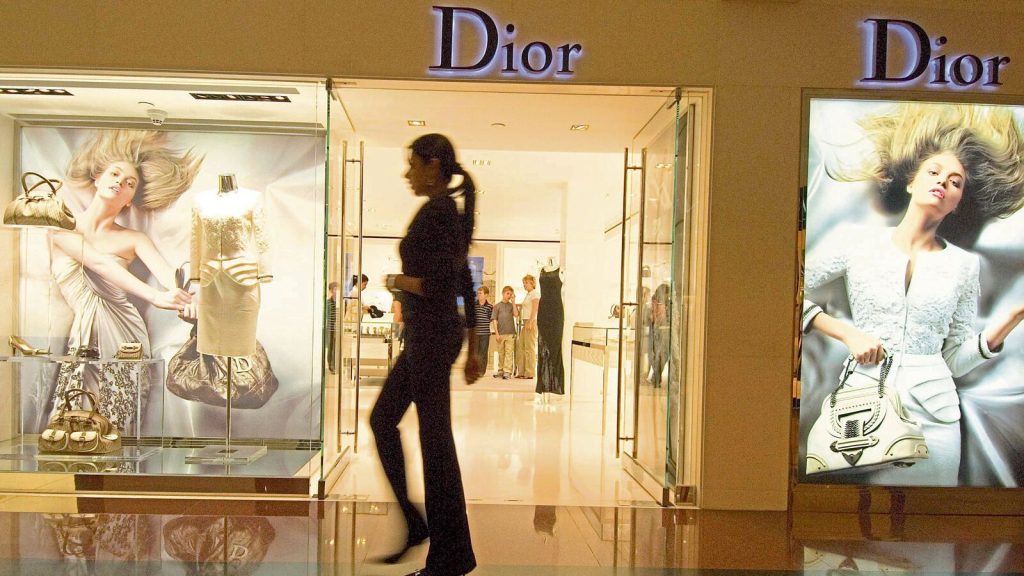

Historically, luxury brands have increased their prices at a rate double that of overall inflation. However, during the pandemic, the demand for luxury goods was so robust that brands were able to raise prices even more aggressively, outpacing their own cost increases. For instance, the price of Christian Dior’s medium Lady Dior handbag has skyrocketed from €3,900 in 2020 to €5,900 today—a staggering 51% increase—while the cost of production has only risen by 18%. This disparity has led to consumers paying 15 times the manufacturing cost, up from 12 times just a few years ago.

While higher prices have bolstered profits for some brands, they have also made consumers more discerning about their purchases. Shoppers are increasingly inclined to invest in brands that they perceive as offering superior quality, often bypassing those that do not meet their expectations. This flight to quality has benefitted high-end names like Hermès and Brunello Cucinelli, which maintain a strong commitment to in-house manufacturing.

Shifting Spending Patterns: Jewelry vs. Handbags

As consumers reassess their spending habits, they are gravitating towards categories that offer better value for money. Luxury jewelry, for example, has not seen the same level of price increases as handbags, which may explain why brands like Cartier owner Richemont have fared better in the current climate. Recent data indicates that U.S. luxury consumers spent 2.6% more on jewelry in September compared to the previous year, while spending on designer handbags plummeted by 13%.

The Rise of Challenger Brands and the Resale Market

In response to the changing dynamics of the luxury market, challenger brands are emerging to fill the void left by traditional luxury labels. Mid-priced handbag brands such as Polene, The Curated, Cuyana, and Ateliers Auguste are gaining traction among Gen Z consumers, who are more skeptical of luxury than previous generations. These brands offer products priced between $300 and $700, appealing to a demographic that seeks quality without the exorbitant price tag.

Simultaneously, the resale market is thriving as consumers look for ways to acquire luxury items without paying full retail prices. The resale business has grown three times faster than the primary luxury market since 2019, with platforms like The RealReal reporting an 11% increase in sales in the third quarter of this year. This growth is particularly notable in the luxury handbag segment, where consumers are seeking options in the $1,000 to $3,000 range—an area where the primary market offers limited choices.

The Future of Luxury: Balancing Exclusivity and Accessibility

As luxury brands grapple with the loss of entry-level shoppers, some industry leaders argue that maintaining an exclusive image is paramount. LVMH’s financial director, Jean-Jacques Guiony, recently stated that introducing affordable products would be a mistake, emphasizing the importance of staying true to the brand’s identity. This perspective suggests that luxury giants may be willing to sacrifice a portion of their customer base to preserve their brand prestige.

However, this strategy could backfire as rival brands eagerly step in to capture the millions of consumers left behind. The luxury market is at a crossroads, and how brands respond to these shifts will determine their future success. As the landscape continues to evolve, the interplay between exclusivity, accessibility, and consumer preferences will shape the next chapter of luxury consumption.

For Sale! 2016 Sea Ray 350 Sundancer – $180,000

Reel Deal Yacht is pleased to feature a meticulously maintained 2016 Sea...

Chinese Couple Opts for Bicycles Instead of Limousines for Their Wedding, Earning Community Blessings

A Unique Wedding Journey: The Bicycle Wedding of Xing and Her Husband...

Luxury platform Trenby announced on the 26th the launch of its new “Trenby Auction” service, which…

Trenby Auction: Revolutionizing the Luxury Goods Market In a significant move for...

Braman Motors Unveils Bold Mixed-Use Campus Redevelopment Plans in Miami’s Edgewater

Braman Motors’ Ambitious Redevelopment of the Edgewater Campus Braman Motors is embarking...

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Alex Palou makes history as 1st Spanish driver to win the Indianapolis 500

Alex Palou took the ceremonial swig of milk in victory lane at...