Why Jet Fuel Is Outpacing Gasoline: How Disruption in the Strait of Hormuz Is Reshaping Markets

As the travel season gains momentum, jet fuel has emerged as the most volatile of refined fuels. Recent disruptions in the Strait of Hormuz—an artery for Persian Gulf crude and refined products—have reverberated through global markets. The result: jet-fuel prices have climbed faster than gasoline or diesel in many regions, even while U.S. production remains strong.

How the Strait of Hormuz shapes global jet-fuel supply

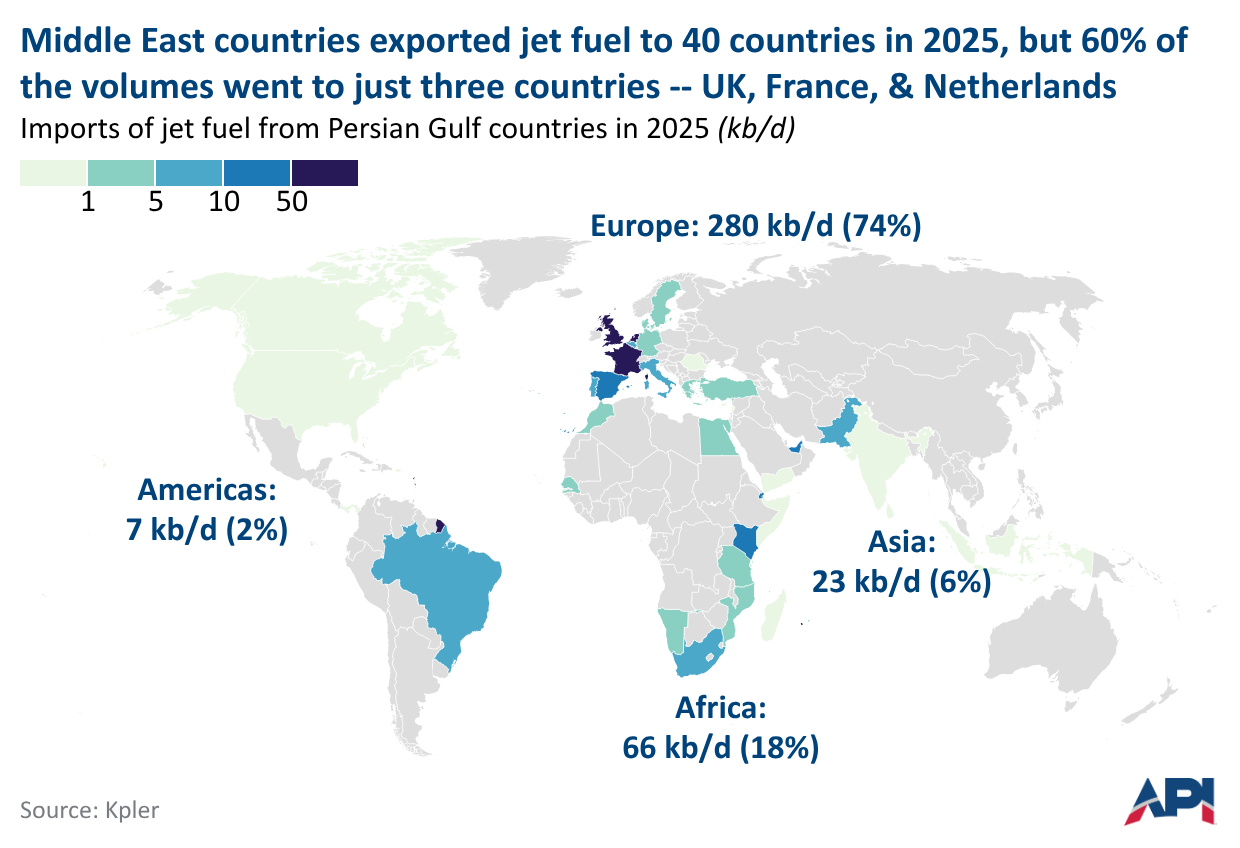

Countries in the Persian Gulf perform two distinct functions for jet-fuel markets: they export a meaningful share of seaborne jet fuel and they supply crude oil that is processed into jet fuel by refineries—particularly in Asia. Before the conflict, refineries in the Persian Gulf accounted for roughly 20% of the world’s seaborne jet-fuel exports, about twice their share of seaborne diesel. When exports through the Strait were disrupted, those flows effectively stopped, and regions depending on those barrels felt the impact most acutely.

Asia’s refining hub is another piece of the puzzle. An estimated 40% to 60% of the crude oil processed by refineries in China, South Korea and India—crude that was then turned into jet fuel and exported—transited the Strait of Hormuz. With that crude curtailed, Asian refineries trimmed runs and reduced exports of jet fuel, tightening supply to other markets.

Jet fuel is a small—yet critical—slice of the barrel

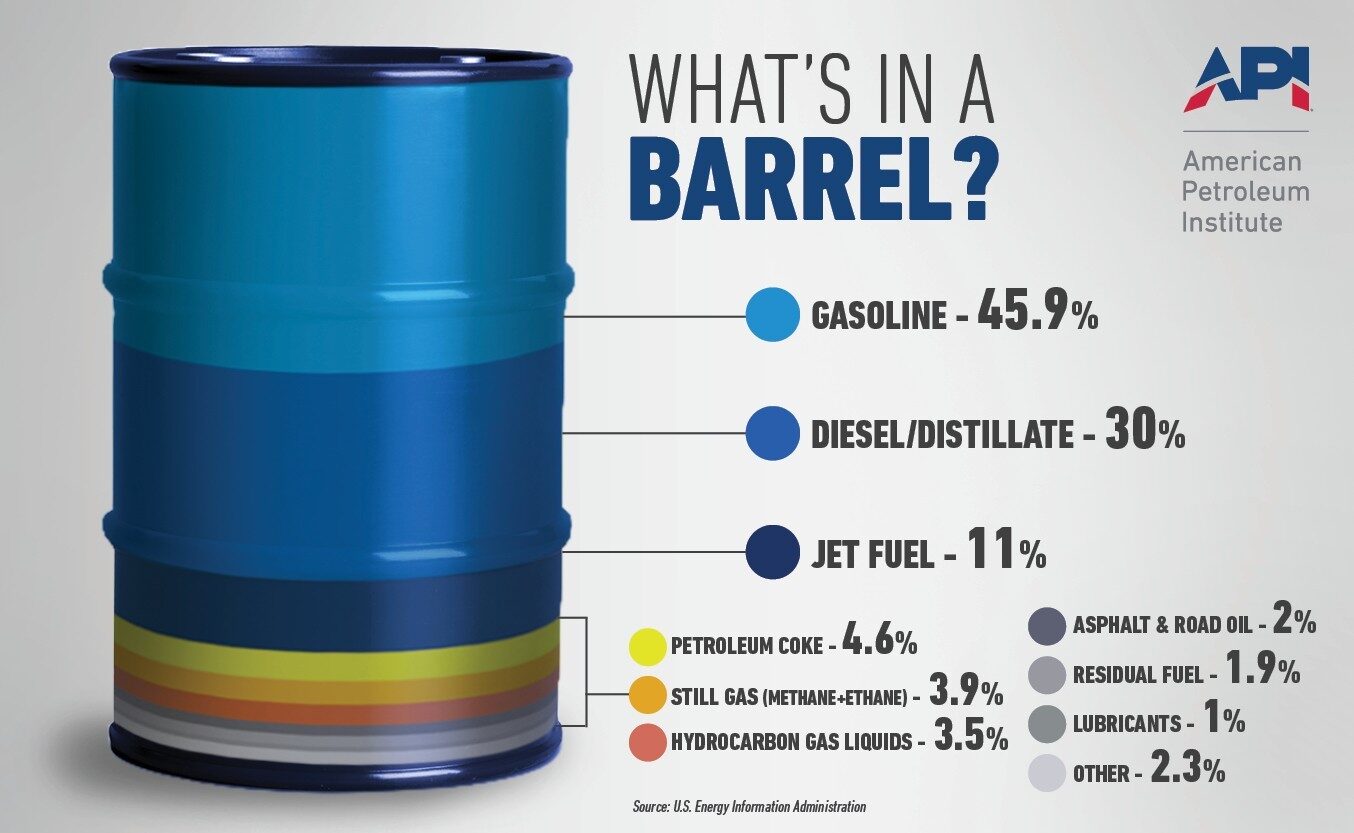

Refining constraints amplify the problem. According to U.S. Energy Information Administration data from 2025, an average barrel of crude refined in the United States yields about 19.3 gallons of gasoline, 12.6 gallons of diesel (distillate) and only about 4.6 gallons of jet—roughly 11% of the barrel. Refinery units are configured to produce particular products; for example, a fluid catalytic cracker primarily makes gasoline and can only be adjusted so far to add jet fuel output.

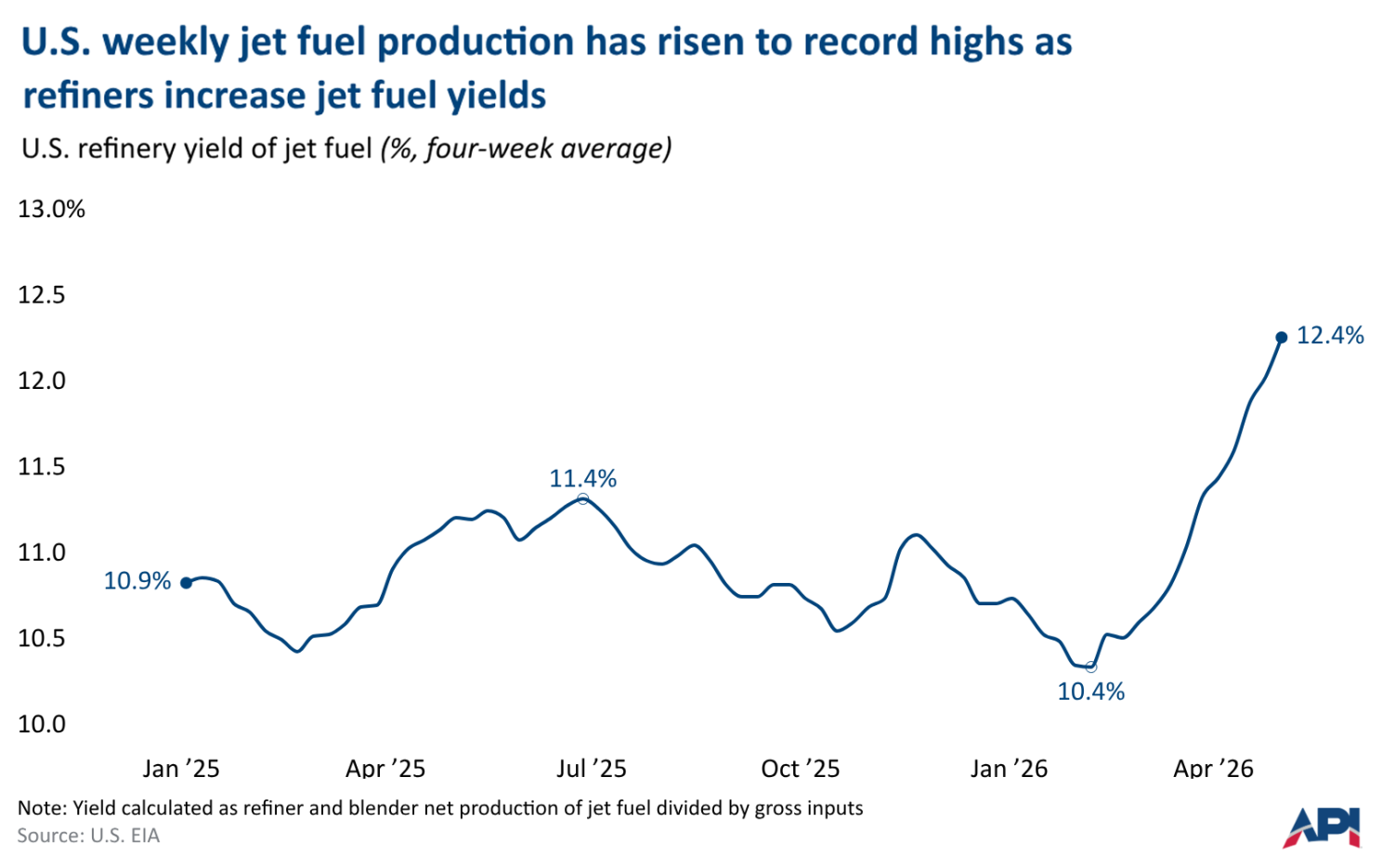

That limited flexibility means refineries can’t simply shift large volumes of production into jet fuel. In the U.S., refiners have managed only modest increases in jet output—on the order of 2% to 4%—leaving markets vulnerable when a significant external supplier is removed.

The United States: better positioned, not immune

The U.S. benefits from being the world’s largest crude producer and from operating one of the largest refining systems, importing little crude or jet fuel directly from the Middle East. That structural strength makes the country less exposed than Europe or parts of Asia. Yet jet fuel is a globally traded commodity, and prices here have been influenced by international dynamics.

The U.S. West Coast provides a concrete example of that connectivity. States such as California rely on imports for roughly 20% of their jet-fuel supply—much of it sourced from South Korea, whose refineries in turn depend on Middle Eastern crude. Strong domestic production enhances resilience, but it cannot fully insulate regional markets from disruptions occurring half a world away.

What this means for summer travel and aviation

With seasonal demand rising, constrained seaborne exports and limited refinery flexibility, jet-fuel markets are susceptible to price shocks that feed directly into airline operating costs and route economics. Regions more dependent on Middle Eastern crude and refined exports—most notably Europe and parts of Asia—face the most immediate pressure, while pockets of the U.S. market show vulnerability where import reliance exists.

Key highlights

- Persian Gulf refineries produced and exported about 20% of the world’s seaborne jet fuel prior to the disruption—roughly double their share of seaborne diesel.

- Approximately 40%–60% of the crude processed by refineries in China, South Korea and India—crude that became exported jet fuel—transited the Strait of Hormuz.

- An average U.S. refinery barrel (2025 EIA data) yields ~19.3 gallons gasoline, ~12.6 gallons diesel and ~4.6 gallons jet—jet equals roughly 11% of the barrel.

- U.S. refineries have increased jet-fuel output only modestly—about 2%–4%—because many units are optimized for gasoline or other products.

- The U.S. imports about 20% of West Coast jet fuel, much of it from South Korea, linking regional supply to Middle Eastern crude flows.

For market participants and operators planning for the peak travel season, these structural constraints underscore the importance of inventory management, alternative logistics and pricing strategies. The American Petroleum Institute’s American Energy Snapshot provides continued data on production, inventories and market movements for those tracking developments.

In sum, the current spike in jet-fuel prices is a function of concentrated supply interruptions and limited refinery flexibility rather than broad downstream demand alone—an important distinction for anyone watching aviation economics this summer.

Make publications with A Bit Lavish in Miami, Florida. Contact us at 305-332-1942

Ann H. (Knight) Meme Capuano Passes Away, Leaving a Lasting Legacy

The passing of Ann H. (Knight) Meme Capuano is a poignant reminder...

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

$8 Million Settlement Proposed in Major Beef Price-Fixing Case

This settlement reflects growing scrutiny over food pricing practices, impacting global supply...

{kind=link}

WordPress 7.0: Are Any of the New Features Worth Getting Excited About?

WordPress 7.0 is shaping up to be one of the most significant...